By Joshua Harrison November 21, 2025

In the current era dominated by digital payments, retailers are confronting the challenge of increased sales costs with fortitude. Whenever a customer pays with a credit card, the retailer is charged a fee, which can vary widely from 2 to 4 per cent depending on the card type. The processors not only take away a part of the profit margin of the small and medium-sized businesses but also drain their pockets of thousands of dollars a year. Therefore, the problem seems to be straightforward though crucial: what is the way out for the merchants to lessen the cost of card payments without compromising the customer experience?

The two leading solutions presented are credit card surcharging and cash discounting. Both approaches can be termed as the means for the retailers to either level out or exclude the credit card processing fees, but they are not identical. Every method commands different legal conditions, customer reactions, pricing strategies, and profit issues. Making a wrong choice may result in legal issues or even losing customers, while the right one could instantly enlarge the boundaries.

This extensive guide below not only presents a very thorough analysis but also assists the shop owners in knowing the ins and outs, advantages, hardships, legal compliance, and perfect situations for credit card surcharging versus cash discounting. We will also analyze real-life examples, provide useful tips for success, and determine factors to ensure that you select the model that most elegantly suits your business.

Merchants Surcharging Credit Cards and Discounting Cash- Why They Are Considered That Way

Even before going through the operations of the two models, it is necessary to realize that, in the first place, the reasons businesses are studying these tactics are profits.

1. The Increasing Expense of Card Acceptance

One can hardly imagine a world without credit cards today. Customers do expect their payments to be easy, and their cash supply is getting lower. But this easy way of paying comes with a cost:

- Interchange fees keep going up

- Visa and MasterCard premium and rewards cards lead to higher processing costs

- All payment networks have their specific fee schedules and do regular updates

- Consumers are getting used to using their contactless payments over other methods

A company that does $50,000/month in credit card transactions will lose $1,450 every month just because of the 2.9% fee, which adds up to over $17,000 per year.

2. Competition and Margin Reductions

Retailers, convenience stores, service providers, restaurants, and e-commerce retailers all work on very tight margins. The practice of absorbing the entire payment fees and not passing them on to the customers is not sustainable over time.

3. Price Pressure

Stores want to remain competitive while keeping prices attractive. Transferring card fees to customers—either directly through credit card surcharging or indirectly through cash discounting—is a practical solution that does not involve raising menu or product prices for everyone.

Understanding Credit Card Surcharging

1. What Is Credit Card Surcharging?

Credit card surcharging refers to the practice of charging a small fee—typically ranging from 2% to 3%—to a patron’s invoice who has opted for credit card payment. The fee thus charged will be the payment acceptance cost.

Key Points of Credit Card Surcharging

- Surcharges can only apply to credit card transactions.

- Surcharged payments cannot be made via debit and prepaid cards.

- Customer awareness is a must concerning the imposition of charges.

- The fees charged should not be more than the exact cost incurred by the seller for processing the payment.

- In several areas, a 3% charge is the limit.

2. How Credit Card Surcharging Works in a Store?

Let us consider a scenario where a customer is purchasing goods worth $100.

- If he/she pays in cash or via debit, then the total remains $100.

- However, in the case of a credit card payment, an additional surcharge of 3% will be applied: $103.

The merchant receives the extra $3 towards the credit card processing fee.

3. Example of Credit Card Surcharging

A nearby auto repair service observes that 85% of its clientele uses credit cards for payments. The processing fees are a monthly $2,000 charge for the owner. By introducing a 3% surcharge:

- Total credit card processing fees are reduced considerably.

- Profit margin goes up.

- Consumers who are cardholders choose to pay the surcharge for the sake of comfort

The mentioned businesses—from beauticians to accountants—are all practising this model successfully.

Benefits of Credit Card Surcharging

1. Reduces or Eliminates Processing Fees

The business passes on the processing fees to the customers who pay using the more expensive payment method instead of absorbing them.

2. Keeps Base Prices Competitive

There is no need to increase your listed prices for all; only credit card customers pay more.

3. Customers Accept It in Certain Industries

There are very few complaints in such service sectors, specialized stores, and professional offices since customers already presuppose high overheads.

4. Easy to Automate

Modern Point of Sale (POS) systems would easily handle it.

Comprehending Cash Discounting

1. What is Cash Discounting?

Cash discounting refers to the practice of reducing the price of a product or service in case customers pay for it in cash. The very essential difference between this and surcharging is that this model does not add a fee for card payments—it simply pays cash users.

2. Cash Discounting: Are the steps to be taken?

A merchant displays a price that is “regular” and that is high because of the cost of accepting cards. The customer pays:

- Full price if the customer is using a credit or debit card.

- Cash payment is incoming through the discounted price.

3. Cash Discounting Example

A convenience store has a drink for $2.09 as its selling price.

At checkout:

- $2.09 is your cost if you use a card.

- $1.99 is your cost if you pay with cash, and that is a discount.

The store will not charge the customers anything extra because it is going to pay the fees for card transactions.

Cash Discounting Advantages

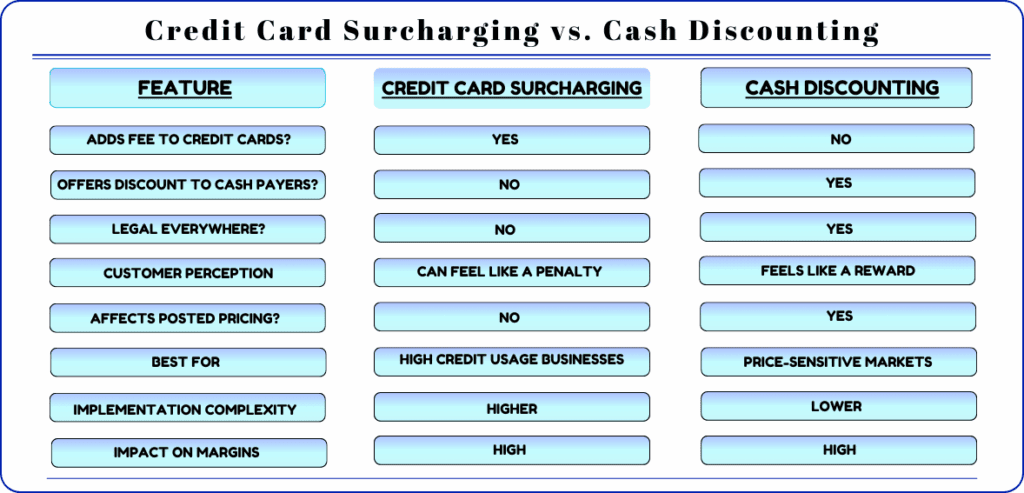

1. Legal Everywhere

Unlike surcharging, cash discounting is legal in all states and in many countries, giving it a worry-free status.

2. Discounts Are Forgiven, Not Fees

Behavioural psychology tells us that people get more positive feedback from “You save money” than they get from “You pay extra”.

3. More Cash Payments

The customers paying cash may benefit the business through:

- Lower fees

- Faster checkout

- Less chargeback risk

4. Simplicity in Compliance Rules

There is no need to apply to card networks or abide by surcharge caps.

5. Perfect for Retail and High-Volume Stores

Cash discounting is prevalent in gas stations, grocery stores, and convenience stores.

Cash Discounting Disadvantages

1. Necessitates Higher Prices Posted Regularly

To give a discount, the base (credit) price has to be a little higher.

2. Customer Confusion Is Possible

Customers might have inquiries like:

- “Why is the sign showing two prices?”

- “Is this a surcharge?”

The significance of clear communication is emphasized.

3. Cash Handling Cost

Handling cash brings along:

- Cost of bank deposits

- Security risks

- Display of time counting money

4. Not Preferred in Luxury or Premium Retail

Dual pricing might not be an issue for upscale or boutique brands if their premium image is not affected.

Credit Card Surcharging vs. Cash Discounting: Key Differences

Below is a clear side-by-side comparison to help retailers understand the distinction.

Customer Experience and How Shoppers Respond

The comprehension of customer psychology is of utmost importance. Customer Reactions to Credit Card Surcharging:

- More or less acceptable when the fee is small and disclosed.

- Industries like repairs, legal services, and medical clinics have this expectation.

- Customers in low-price retail environments may get annoyed

Customer Reactions to Cash Discounting

- Regarded as fair because “cash is cheaper”.

- Supports positive behaviour.

- It is effective in the areas where cash is still in use and is a common practice among consumers.

Real-World Credit Card Surcharging and Cash Discounting Examples

Example 1: Auto Repair Shop – Credit Card Surcharging

Thomas runs an auto repair shop and has to pay card fees of almost $2,400 each month.

However, once he put up a 3% surcharge:

- He had to pay 30% less in fees

- Customers believed in the justifications

- Gain in profit margins was instant

Example 2: Convenience Store – Cash Discounting

A busy convenience store became a cash discounting store:

- 40% of customers started paying in cash

- Costs associated with credit card payments were reduced significantly

- Prices posted continued to be competitive

Legal Requirements: Credit Card Surcharging and Cash Discounting

Credit Card Surcharging Compliance Rules

- Maximum charge: in most cases, 3%

- Notification to card networks must be given 30 days before commencement

- Strict adherence to receipt formatting

Signage must be displayed at:

- Entrance

- Cash registers

- Online checkout pages

Cash Discounting Compliance Rules

- No official caps apply

- No network registration

- Just clearly label the card price and cash price

Choosing Between Credit Card Surcharging vs. Cash Discounting

Select Credit Card Surcharging When:

- More than 70% of customers pay by credit card

- You prefer to maintain low posted prices

- You desire the easiest pricing structure

- Your business is service-based

Select Cash Discounting When:

- Your customers are sensitive to price.

- You want a legal, easy solution.

- You want to promote cash payments.

- You are in the fuel, grocery, retail, or convenience sectors.

Implementation Tips for Both Models

For Credit Card Surcharging:

- Train the staff on how to explain the reflected fee

- Post notices that are easy to see

- Make the surcharge a little bit

- Install POS systems that self-manage compliance

For Cash Discounting:

- Price tags should be clear on the shelf

- Present both prices: “cash price” and “card price”

- Treat savings as a promotion

- Have the staff trained in dual pricing

Final Verdict: Credit Card Surcharging or Cash Discounting?

Credit card surcharging and cash discounting, in the same way, are effective methods of recovering or even eliminating processing fees from the business. The choice is a matter of clientele, pricing, and the business nature.

- If you have a customer base that finds convenience and is financially equipped, then credit card surcharging might be the way forward to offset costs.

- On the other hand, if you are dealing with a price-sensitive and cash-preferring clientele, cash discounting shall raise the margins while satisfying the customers.

No matter which model you go for, a correct implementation may appreciably increase your store’s profitability—most likely within the initial month.

For most stores, cash discounting is the better option as it is less complicated to implement, legal in every state, and frequently accepted by customers. Surcharging is a fee for card use that is legal in a number of states. But it has stringent rules, requires prior notice, and can even put off customers, making it a less attractive option for many retailers, particularly in some areas. Cash discounting provides an incentive for paying by cash, while surcharging imposes a charge on card purchases.

FAQs

1. Is credit card surcharging legal for all businesses?

Ans: Yes, it is. As credit card surcharging is permitted in most states in the United States, it is strictly controlled. Business owners should always consult the up-to-date local regulations before applying any surcharge programs.

2. Does cash discounting help reduce the processing fees?

Ans: Yes. Cash discounting permits businesses to give a discount to customers who pay with cash while keeping the card prices slightly higher to cover the processing fees.

3. Will surcharging or cash discounting upset customers?

Ans: Surcharging or cash discounting is based on the customer demographic and how you advertise the program. A large number of customers have encountered convenience fees and cash discounts, particularly in the sectors of gas stations, restaurants, and retail.

4. Which program is better for small businesses- surcharging or cash discounting?

Ans: Small businesses that aim to reduce processing fees are most likely to opt for cash discounting. The best option that really depends on the customer behaviour, the average size of the ticket, and the price sensitivity of your market.

5. Is it possible to have a surcharging and cash discounting program at the same time in a single store?

Ans: No, businesses are obliged to select a single compliant program. The combination of both will lead to confusion regarding pricing and will be against the card-brand rules.